The Future of FinTech is DeFi Native, resistance is futile. Part II

The Future of FinTech is DeFi Native, resistance is futile. Part II

The biggest risk to big banks and traditional finance is people simply opting out for self-banking. The answer is obvious.

Last week, in part 1, I wrote:

Tech companies will differentiate themselves by integrating smooth core product experiences with [open] finance. The best will tailor their products to integrate with the growing investing as entertainment culture in a way that is transparent, equitable, and entirely portable across their competitors.

Here, in part 2, I want to focus in on portability, transparency, equity, and how they parallel with open source software that is already the gold standard in tech. Through this, I’ll describe how FinTech companies can copy this open-finance native design to support and generate value-add to the future of self-banking.

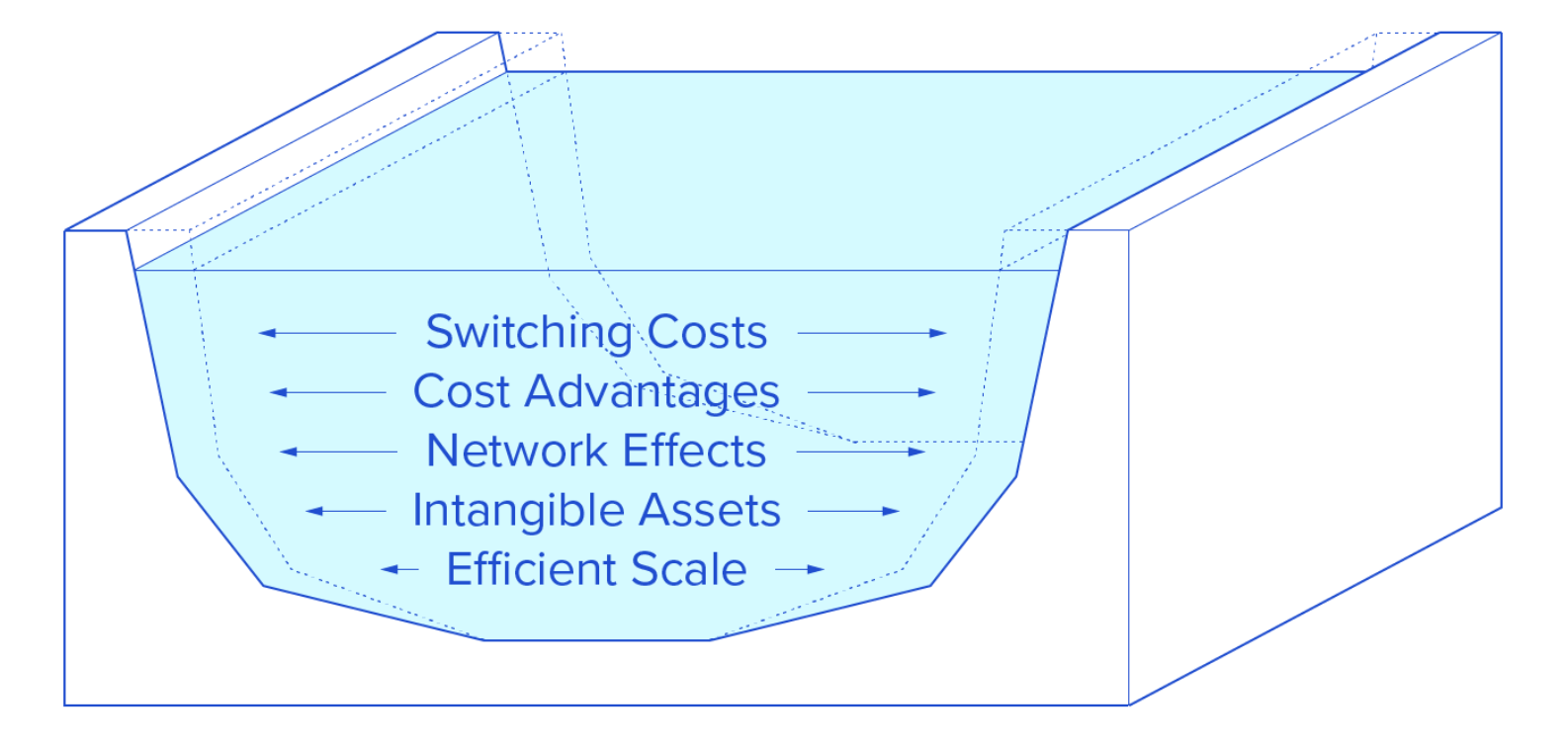

There’s a phrase- every company is a tech company. The idea is that corporations have shifted from IT/data/tech being a cost of doing business to being a key capability and driver for growth. It’s no coincidence that the companies best at collecting, storing, analyzing, and using customer data are growing faster and bigger than their competitors. More data provides network effects:

The more customers you have >

The more data you get >

The better you’ll get at getting new customers >

Which will get you even more data >

Repeat 1-4 until you have an economic moat.

Let’s hone in on Amazon and their economic moat in cloud computing. Amazon Web Services (AWS) has almost 1/3rd of the entire global market for cloud computing. That’s crazy. How are they doing it?

They integrate with and contribute to open source software.

Check out AWS’s page on their open source contributions. Why would they use community driven programming languages and applications that explicitly allow anyone to use, study, dissect, copy, change, and redistribute the code behind software to anyone else for any purpose? Where’s the profit?

They recognize their value comes from value add not from value locked.

This may go over some heads but it’s ok if you only partially get it.

AWS provides cloud services, such as virtual machines. What you put onto their virtual machines is up to you. There are numerous open source offerings like Docker that contain pieces of a large application into modular chunks to make working with these virtual machines feel like playing with fancy Legos.

Modern DevOps (i.e. how software is built and managed today) use these containers because they are transparent and portable. You know exactly what the containerized piece of your app will output given specific inputs. The container can live in any environment that meets relatively common and standardized conditions (i.e. on AWS, or on Microsoft Azure, or on Google Cloud platform, or locally on your laptop).

By providing integrated user interfaces and user experience to complex, but open source/portable/transparent/community-driven software, AWS provides significant value-add without profiting from your misery through vendor-lock.

They eat their dog food.

By using their products and experiencing the open source world directly they build an internal customer perspective that allows them to solve customer problems before the customers are even technologically savvy enough to have the problem. Here’s a (long) video from 2017 describing how they use AWS to manage the retail wing of Amazon, including how they spent years building products internally before launching them publicly.

Okay, enough Bezos worship lol. My point is not that Amazon is the best or anything. My point is they’ve succeeded in the 3 steps of collaboratively profiting from open source programming. FinTech has 3 parallel tasks to collaboratively profit from open source / decentralized finance / self-banking:

Build on top of, not in place of, open source / decentralized finance.

Decentralized finance protocols like AAVE (lending/borrowing), Uniswap & Sushiswap (Liquidity between assets using AMMs), and Alchemix (self funded annuities) generate real cash flow and investment opportunities but can feel overwhelming to figure out for an newbie.

Everything from storing private keys to knowing which protocols are safe to knowing how to navigate Web 3.0 compliant web pages to approving tokens / adding liquidity / staking / yield farming / etc. just feels complex and not digitally native the way messing with a well designed mobile app feels.

User experience is just not mature in this space.

FinTech’s emphasis on wrapping traditional finance first (i.e. stock markets and savings accounts in a nice mobile app) is misguided- there isn’t any money in copying the inefficiencies of traditional banking! This shift to open finance native will be liberating for their both their operational efficiency and data science.

Focus on the value-add not the value locked.

FinTech applications bring user experience, human centered design (HCD) interfaces, customer service, account management, and yes, useful regulation to the chaotic middle ground of crypto and traditional finance.

But they do it in a way that focuses their moat building almost entirely on switching costs. Including not allowing switching in the first place!

When you buy some Ether on most of the major FinTech apps (at time of writing) you’re almost always just buying a receipt for a piece of their Ether pile. It is only recently becoming more demanded by users that they be allowed to own the Ether directly, i.e. being able to move the coins out of the FinTech pile and into their own custody on the Ethereum network.

Not only should FinTech allow this, but they can automate a lot of management overhead by simply being native to these networks and working with the existing protocols (via APIs or their own custom smart contracts) to make real ownership (and thus portability) the standard. All while generating significant revenue through their value-add.

Get your hands dirty and try out these protocols as a user.

FinTech will better understand how to add value through UI/UX and custom product offerings layered on top of a transparent, portable, accounts by actually using the products!

When they are generating revenue from interacting with DeFi protocols (i.e. paying an internal DeFi team that puts a significant % of their private reserves to work) they will naturally develop the procedures, tools, and skills to bring the best strategies (risk adjusted of course) to their customers.

Ok, so hopefully the parallel makes sense across both traditional tech and future finance: build on, not instead of, open source; Focus on adding value not extracting it; prove it works for you before you try and sell it to your customers.

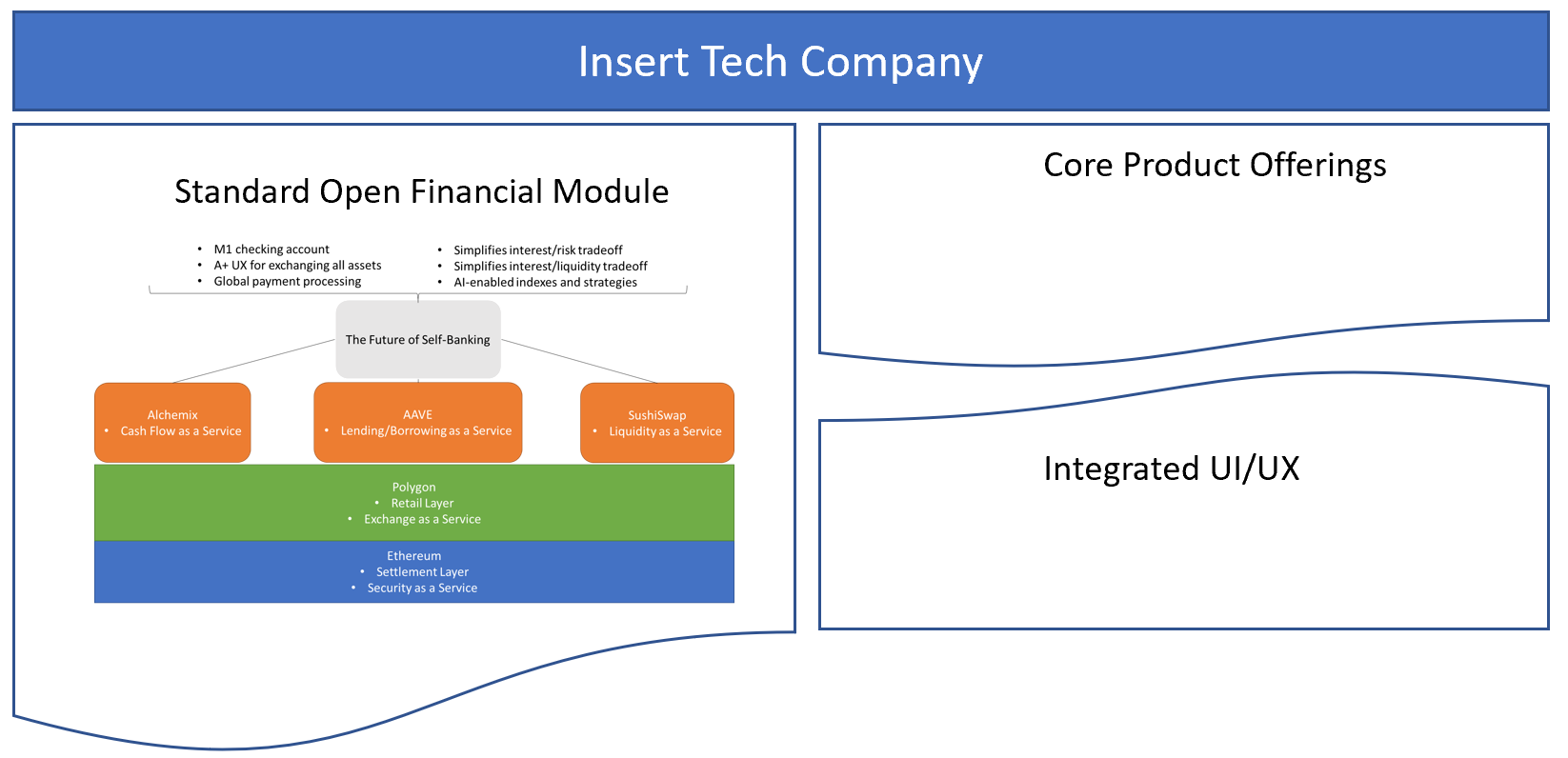

Let me break down an example architecture for a DeFi native FinTech company. Note, if this feels very complicated, it is, but I’ll try to highlight the things the user notices versus what the company handles.

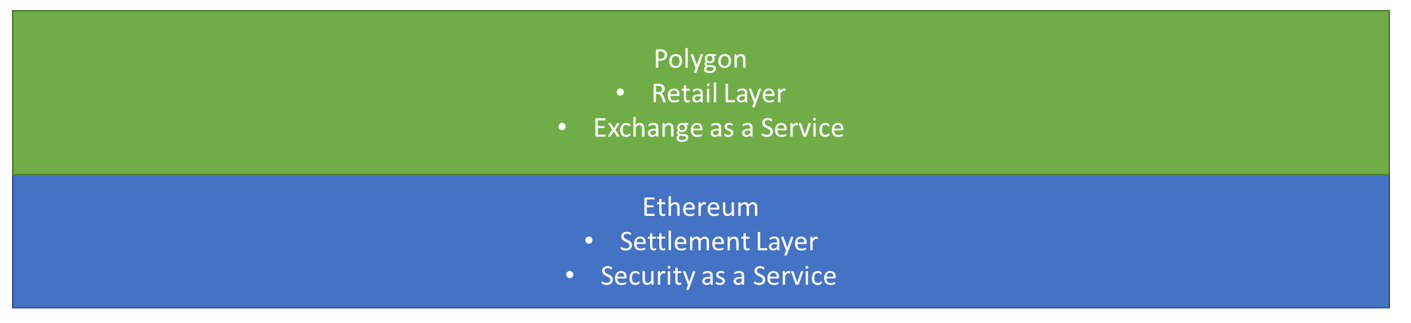

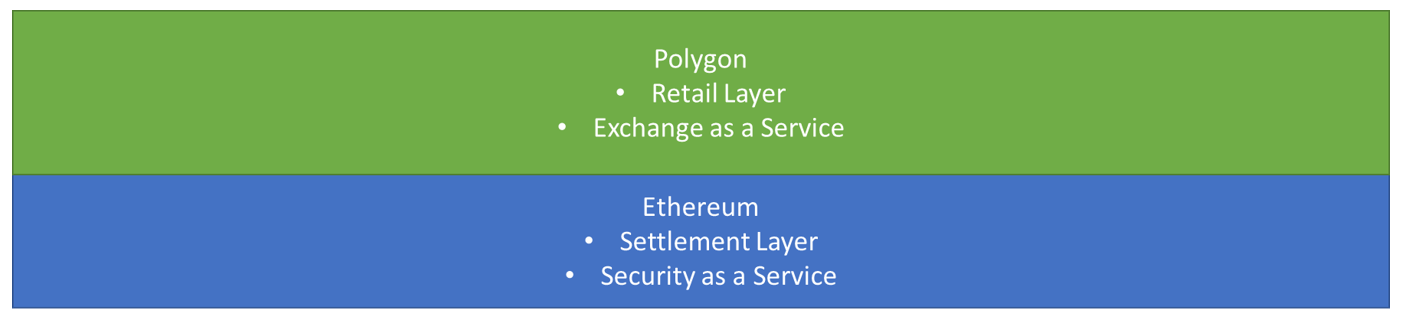

The Security Layer

FinTech can use the Ethereum blockchain to serve as decentralized record keeping of all accounts. This Allows savvy consumers to natively port their funds to (and from!) competitors through direct ownership of their wallets.

When a user signs up, they don’t just sign up for your company, you actually generate an account for them on the blockchain including giving them access to the private keys, seed phrase, and other relevant information so they can take their account wherever, whenever.

The user should start out completely abstracted away from this, but there should be clear documentation and instruction for those interested in increasing their control up to and including going all in on self banking. If you make the off-ramp from your products smooth, it actually improves the boomerang effect- people realizing they don’t want to go it alone and appreciated your services.

The Investment Layer

Decentralized finance has hundreds of protocols, tokens, and opportunities. The vast majority are complete garbage. Scams with minimal liquidity, audits, or trustworthiness of users money.

Just like the Internet!

Where scams, malware, malicious websites, run amok. People just trust intermediaries like Google to keep that stuff out of their view.

FinTech should be serving that Google position as a checker of opportunities. Whether it be partnering with blockchain audit firms like QuantStamp or running their own audit teams, they can choose which protocols they enable in their apps. This opens up the door for them to value-add these protocols, including through private insurance of the interactions of those protocols they organize (i.e. 1-click access to protocols that mechanically involve multiple different transactions and security layers). This both exports and limits their exposure to the risk of holding user’s money themselves.

The user should be moderately exposed to this layer.

Like picking a movie on Netflix, where they balance ratings, length, and intro information to pick entertainment- FinTech should make picking investments as simple as balancing risk, reward, liquidity, security, and in terms of UX - what kind of insurance assurances are available based on the FinTech company’s own audits/experience using the protocol internally.

I am not saying the users should be babied. They must, of course, agree that nothing is guaranteed and past returns don’t always reflect future gains. But in terms of black swan events like $200M exploits, there should be a reasonable amount of private insurance available to protect users engaging in risky activity. For example, the FinTech company could charge a fraction of user gains monthly to cover black swan coverage. There are actually already decentralized insurance services like Cover that can support this, but traditional insurance may make sense too.

The FinTech Core Products Layer

This is the layer that the average person actually deals with, at full maturity it would include:

Permissioned/Removable account services, e.g. private key storage. If I want to leave app X, I should be able to cancel my insurance agreements, revoke their access to my wallet, and simply bring my wallet to another service.

A common payment processing standard to any entity globally. Just like you can go to any website via their IP Address or Domain Name Service (DNS, i.e. normal website name) and submit / receive information. You should be able to do the same thing with a wallet address (or ENS) and submit/receive money as information. This includes direct deposit from employers and paying taxes!

Dashboards to track spending across defined categories & investments over time.

Embedded market information for those more active investors.

Fluid levers to control ownership, liquidity, risk, rewards, and just overall documentation and learning about the options available (i.e. the depth and complexity of interacting with the investment layer).

A spectrum of private insurance solutions for protecting against black swan events (i.e. issues out of their control at the settlement or investment layer, not insurance for simple losses lol).

Now of course, this does not cover all banking services. One of the most incentivized financial instruments in the US today for example is undercollateralized lending, i.e., borrowing $100,000s for education or a home with nothing more than a promise to pay it back and maybe some past pay stubs. Decentralized finance does not do undercollateralized loans very well, because it is rife with bias, human judgement, and using the traditional legal system to enforce non-algorithmic contract law (can’t be done in a smart contract).

There is a place in the economy for fully centralized and incentivized banking services. These are the exact kind of services that fall into the value add category of FinTech. But to summarize, here are the things that can and really should be decentralized:

Sending/Receiving money (as information) to make payments

lending/borrowing money with appropriate collateral and liquidation to earn interest revenue.

providing liquidity between assets to earn swap fee revenue.

Agreeing to conditioned payments through algorithmically enforced rules, including but not limited to: flight insurance, stock options, sports betting, private payment agreements (e.g. gig economy), self-funded annuities (cash flow), and many more.

Ok, so I covered portability and the parallel to the already existing best practices in open source (not-finance) software. Let me add two quick points on transparency and equity before I sign off -

When FinTech capitulates and moves to this open source, value-add, self-test model, it will significantly improve data transparency. All FinTech companies will work off the same set of blockchains, doing similar investments, and competing with the same data (including on-chain data about each other!). Check out Dune Analytics to see the kind of data analysis being done by thousands of people on the massive amount of public data available on the $1T+ Ethereum network.

This information symmetry / data transparency will allow everyone to play on an equitable playing field. Yes, large FinTech will have more money for more analysts and earn a bigger share of the liquidity pool swap fees, etc. But it will be proportional and competitive. If they put $1M and I put $1k, they’ll only get 1,000x the swap fees as me. They don’t get a bonus (or a discount on borrow rates) for being larger than me. The kind of benefits that make the gap between us grow. I can take more risks, or do more research, or get lucky and outperform them through self-banking with enough effort. They will be forced to continuously innovate drive additional value-add. Not simply print from value locked and switch costs.

Thank you as always for checking out my off the cuff thoughts, you can subscribe & share here: