Big Tech & Big Banks will comply with DeFi self-banking, resistance is futile. Part I

Big Tech & Big Banks will comply with DeFi self-banking, resistance is futile. Part I

The only reason you aren't self-banking is because all the apps suck, but that'll change.

Here’s some of what the perfect bank would let you do:

Accept direct deposits from employers

Store funds for everyday use (maximum liquidity)

Handle payment processing natively to send money from your everyday use account to retailers, utilities, government, and individuals

Store funds at lower levels of liquidity in exchange for interest

Provide access to a marketplace of investment opportunities

Low cost and near instant exchange between layers of savings liquidity and investments with clear information on the risk tradeoffs.

Track all investments and liquidity levels including relevant KPIs and data visualizations

Enable custom investment plans, i.e. allow you to set your own rebalances, harvesting of interest, etc.

Leverage artificial intelligence to recommend investments based on data you freely provide & can revoke and provide forecasts/market trends & news.

Ok that last one might be pushing it.

But we are so close to this future with decentralized finance. Bankless is a leader in the self-banking space and I highly recommend their initial overview of the skill cube for being a self-banking aficionado if that’s your thing.

While they come at it from an active investing & maximization standpoint- I frankly, am not a maximizer. I have my financial independence target and once I hit that target, I’ll probably massively de-risk my portfolio and just chill off small, stable returns for a few decades. You won’t see me moving to Miami with my bitcoin winnings.

If you’re like me and are just trying to take a bit more control over your investing here’s a brief overview of what I think the near term future of self-banking looks like starting across 3 foundational predictions:

Open source financial protocols will globalize capital flows the way advances in supply chain globalized labor flows.

One parallel in terms of disruption is how open source programming languages combined with an open internet have completely revolutionized entertainment, business to business software (software as a service, vendor-portability), retail, and access to information (e.g., ad-tech and journalism).

With the internet today every institution from governments to corporations to small businesses to individuals has access to a set of common protocols/layers for information exchange.

Money as information simply stacks on top of this with its own open source financial protocols/layers. This is the foundational step for funding the decentralization required to create Web 3.0 - the censorship resistant, peer to peer, globally accessible storage, computation, and transfer of information.

So, clarifying summary.

The future of the internet is decentralization. That’s Web 3.0.

For decentralization to work, you have to have individuals & enterprises opt into hosting and sharing information related to a defined protocol (e.g. a blockchain) and perform calculations, copies, and distributions of the information to anyone making a protocol compliant request.

For people to be incentivized into doing this, you have to pay them for their time, energy and computing costs. For them to trust they’ll be paid, you need to ensure the payment system itself is trustless, i.e., decentralized too.

Thus, solving decentralized money is the first step to transforming the internet from a semi-centralized global marketplace into a fully decentralized global computer.

One major impact from this is it will become exponentially more difficult for single nations to regulate capital flows when the internet itself becomes the primary financial infrastructure not banks, pawn shops, and loan sharks. To control money will require controlling all transfers of data an insane feat even for autocratic governments.

Efforts to control money laundering like know-your-customer laws will face possibly insurmountable difficulties at the granular everyday person level simply from sheer volume of data, but in some ways becomes much simpler with the transparency that blockchain introduces for extremely large accounts that are watched nearly cultishly for market signals (whales).

The line between Big Tech and FinTech companies will fade away. Amazon, Facebook, Apple, and Google will all launch embedded financial applications into their applications, hardware, and/or platforms.

This may include acquisition or partnership with emerging pro-crypto FinTech companies (SoFi, PayPal/Venmo, Square/CashApp, Coinbase, Robinhood, M1, etc.) many of which already have primary banking affiliates like JP Morgan.

These technology companies, already at the cutting edge of planetary software as a service and information distribution will be best positioned to incorporate the open financial protocols that stack on top of the internet.

I suspect this will get too far to reverse before regulators and legislators are able to fully flesh out the implications, making simple expansion of the current set of know your customer and anti-money laundering laws the most probable stop-gap measure.

This will be entirely acceptable to the vast majority of everyday consumers that value centralized customer service and the protection of financial regulation.

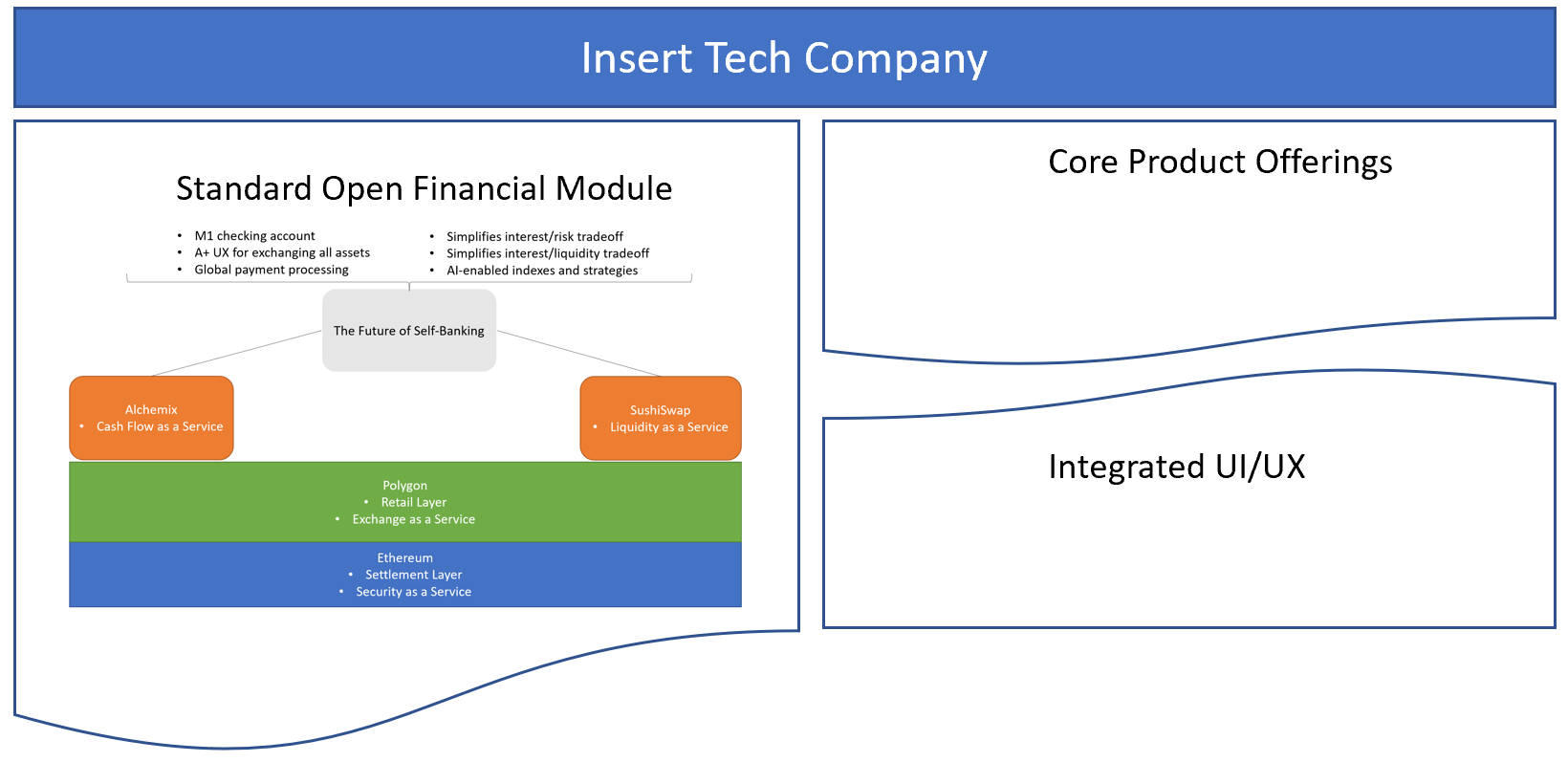

But that doesn’t need to mean their money will be controlled by the company providing the user interface & experience that wraps around the open and decentralized financial protocols.

Some critical regulation I would hope to see implemented would be a combination of net neutrality and financial portability. People should be freely able to port their wallets across tech companies and even revoke access to the data (i.e. their money!) at will.

Tech companies will differentiate themselves by integrating smooth core product experiences with finance. The best will tailor their products to integrate with the growing investing as entertainment culture in a way that is transparent, equitable, and entirely portable across their competitors.

For those of you reading this who’ve never interacted with decentralized finance, this may be a confusing concept.

Don’t you need log-ins? registrations? Wouldn’t the company get to control my account however they want including deleting it or holding my funds?

No, it doesn’t have to be that way.

Decentralized finance already has tools like MetaMask that navigate your account across web 3.0 compliant websites such that they can’t control your money. They can only organize interactions with the protocols (e.g., tabulating how much money you owe someone and providing a button to click to pay them) and then they ping your account to approve the interaction they set up for you.

Imagine a single log-in that proves your identity across all major websites that you allow to see your information and also you can revoke that permission at any time. That’s the promise of Web 3.0.

It’ll be complicated, these sites will realistically centrally manage the private keys (i.e. the log in info) of most of their customers simply because the customers don’t want the stress of a password they’re never allowed to forget. But if we build and regulate it right they’ll need to allow complete user control for those who want control.

This unlocks the future of both self-banking and ownership of your identity on the internet.

I’m getting close to the email size limit here- so I’ll be breaking this into 2 parts.

Here’s the summary for today and look out for part 2:

blockchain/crypto/decentralized finance will be a new layer on top of the internet you know and love

A decentralized money layer on the internet makes it possible to create a decentralized internet (Web 3.0) because you’ll have a means of paying people to opt into anonymously running defined protocols on their machines including information storage, computation, access, and transfer.

Big Tech is in the best position to wrap & integrate this finance layer into high quality UI/UX experiences for those using their products.

Financial regulation should (hopefully) catch up and require a net neutrality / financial portability requirement that enables people take control of their money/information (recall, money will become equivalent to information) if desired.

Here’s what to lookout for in part 2:

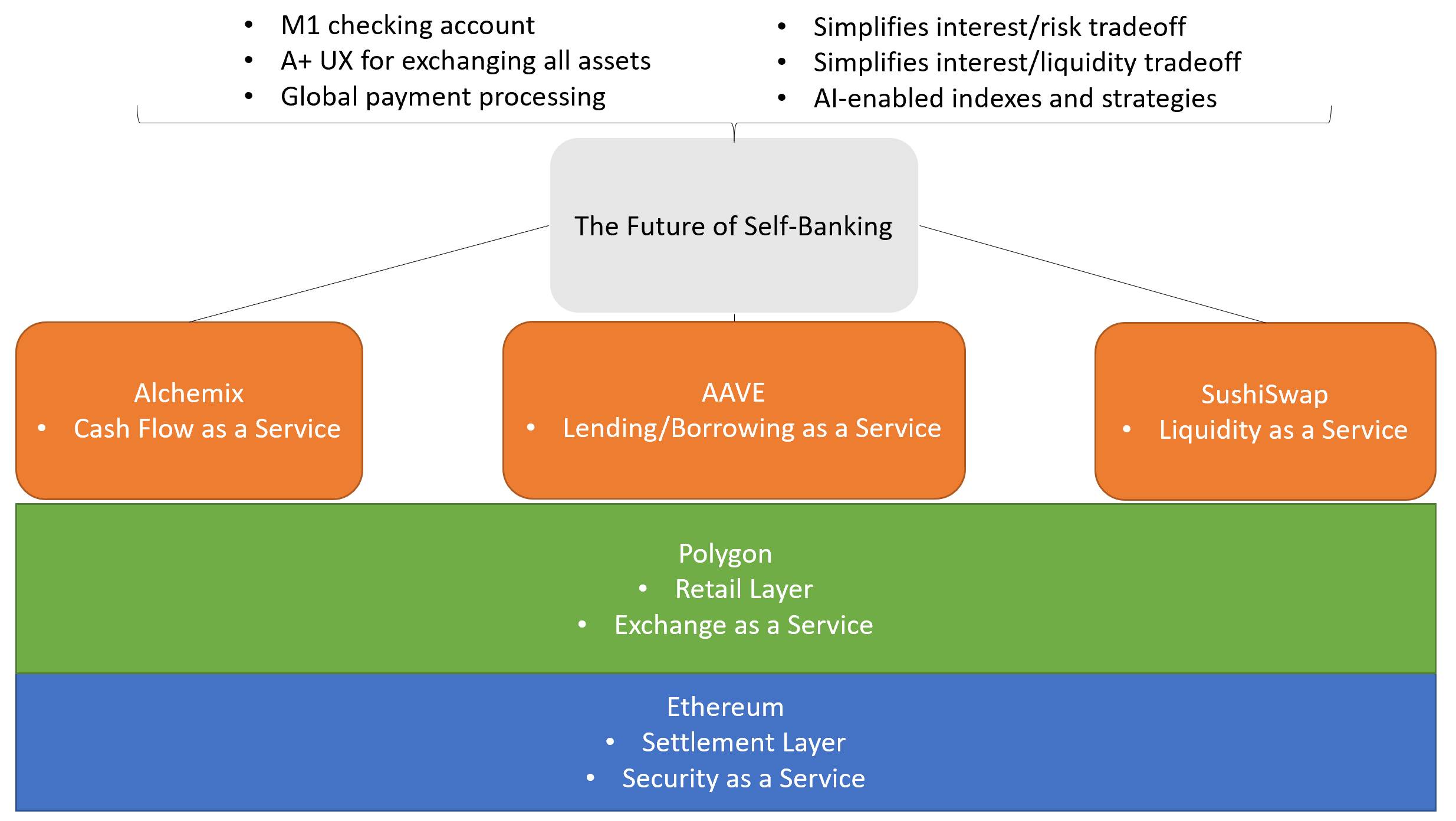

An example architecture for semi-self banking today (complex, but worth understanding).

Key blockchain and smart contract protocols that make up that architecture and how they work.

What I expect will happen to traditional finance investing as self-banking and professional semi-self banking grow.

Thank you for reading, as always you can subscribe & share here.