Generate cash flow and stop buying Bitcoin prayers part II

The rich don't HODL. An intro to cash flow in DeFi.

Yesterday, when I mentioned HODL is an outdated investing paradigm I took aim at the very foundational concept of diamond hands.

More specifically my points were:

The “Buy, hold, wait decades, sell” paradigm only makes sense in highly regulated markets with circuit breakers and distortionary tax policies that ensure consistent demand flow at any price.

That life is complicated and locking away your biggest sack of money for decades has risks and liquidity has value.

In the highly unregulated decentralized finance space there are no mechanisms to stop panic selling, no guarantees of consistent demand flow, and thus it is not reasonable to expect the average person to withstand 30 - 70% price drops overnight and simply say “stop being a paper hands!”.

This last one isn’t a popular sentiment. A lot of the big players in the DeFi space come from anarcho-capitalist and anti-authoritarian leanings. They insist on free markets, do your own research, only putting in what you can afford to lose, personal responsibility, etc. etc.

I am sympathetic to those arguments. But what I care much more about is universal market access to basic financial services.

This is not an argument for regulation. It is an argument for range.

The average person needs a range of risk-reward opportunities that are liquid, with low transaction costs, and low latency. So in this post I want to discuss stablecoins and some of the lower (but not 0!) risk options in DeFi so you can advance out of the traditional HODL investing paradigm into the ideal cash flow investing paradigm. This is not financial advice, it’s purely informing you that these things exist!

A stablecoin is a crypto currency that attempts to maintain a peg to another asset, typically a US dollar.

This provides an “exit” from other crypto assets without fully exiting into the traditional financial system. A few major ones include Bitfinex/Tether’s USDT, Coinbase/Circle’s USDC, MakerDAO’s Dai, and the decentralized stablecoin AMPL.

They have varying histories of success maintaining their peg (i.e. 1 USDC = $1) in periods of high volatility, but for now just know they try to stay worth $1.

There are protocols out there that allow you to lend your coins to others in an decentralized and non-custodial way.

For example, AAVE, one of the major protocols with over $16B in total liquidity for borrowing and lending both stablecoins and a few major non-stable crypto assets (e.g. ETH, BTC).

Quick screenshot to see stats on the big 3 stablecoins including variable rate and fixed rate borrowing. Be honest, is your checking or savings account matching these interest rates? There’s something to be said about automating out all the operating costs of a bank!

Of course, depending on your country, you may have extra perks that validate the reduced interest rate such as having your deposits insured (which reduces systemic risk). In the US, up to $250,000 is insured by the FDIC, essentially removing risk (and reward) from depositing US dollars in a bank.

Another way to put your money to work generating yield in DeFi is via liquidity pools.

In centralized finance, buyers are matched with sellers through an exchange or broker. Because the market is very large and mature it is near instant in most exchanges to buy or sell an asset. Liquidity is a measure of how quickly you can turn your asset into a different asset (usually measured in terms of how quickly to cash).

Selling a house takes time. Even with all cash offers, you still have to do paperwork and get all the legal items sorted out. Selling a baseball card on eBay takes time too, but that’s less legal overhead and moreso waiting for a buyer to come along. Selling an Amazon stock is near instant, because it’s a public company traded constantly on the NYSE. This means houses and baseball cards generally have less liquidity than Amazon stock.

In crypto, there are centralized exchanges like Coinbase that bring that instant liquidity through centrally managed matching of buyers & sellers. But for decentralized finance to be decentralized, buys & sells can’t go through a single company.

The most popular solution is called automatic market makers (AMMs). I won’t dive into the details here. The core principal is- create a pool of funds between 2* assets and allow anyone to buy and sell either asset to these pools. Essentially automatic buyers and sellers for any two assets.

(*I’m saying 2, but there are actually protocols like Balancer that allow up to 8, creating essentially a yield bearing, automatically rebalancing index fund. That’s for another post).

If you have (Ethereum network wrapped) Bitcoin but want USDC. You simply go to the wBTC/USDC liquidity pool on a major exchange protocol (e.g. Uniswap or Sushiswap) and give the pool your wBTC and in exchange you get USDC.

In exchange for “liquidity as a service” you cough up 0.3% of your wBTC as a fee to those providing liquidity. The same 0.3% works in reverse for buying wBTC with USDC.

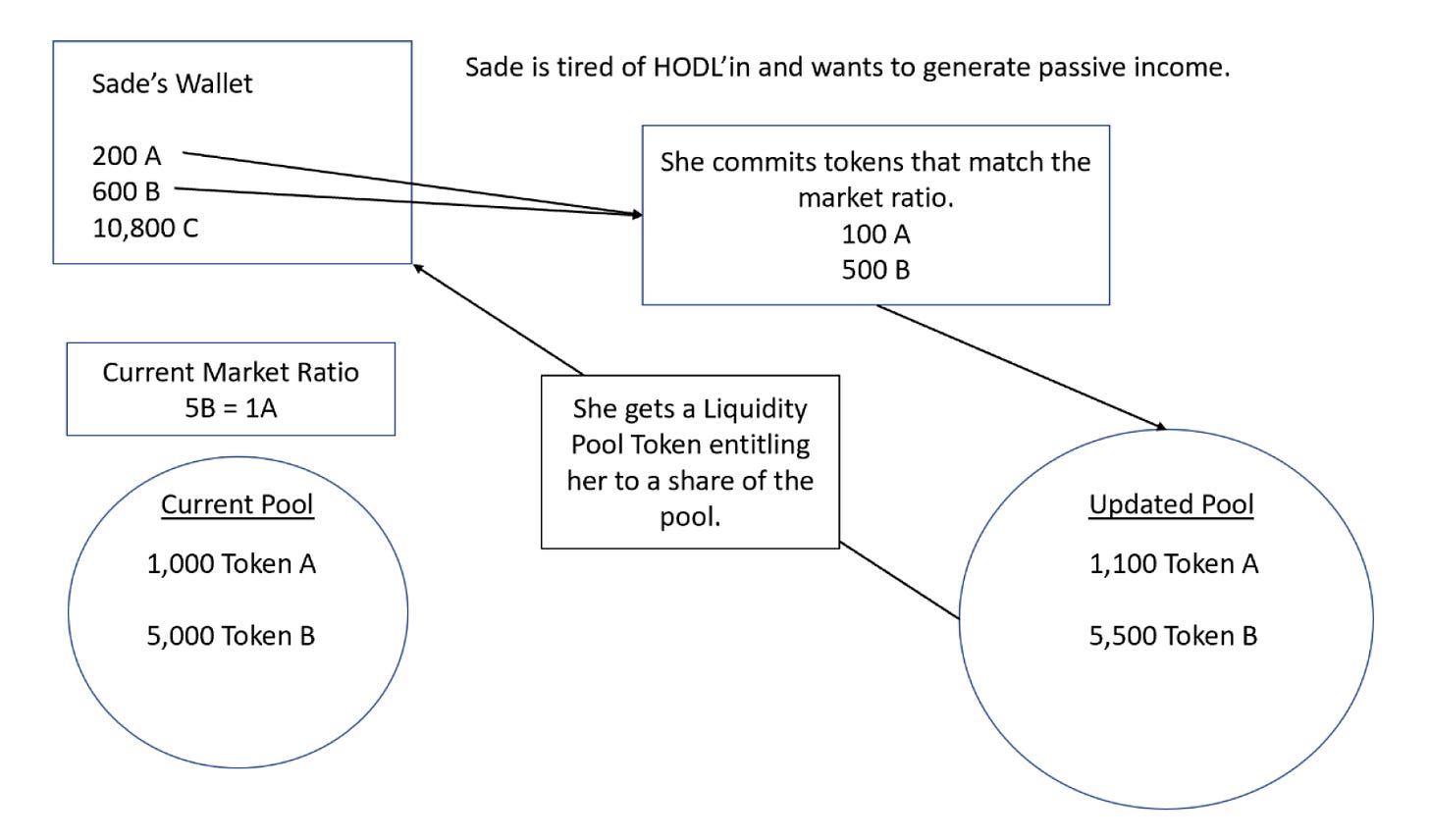

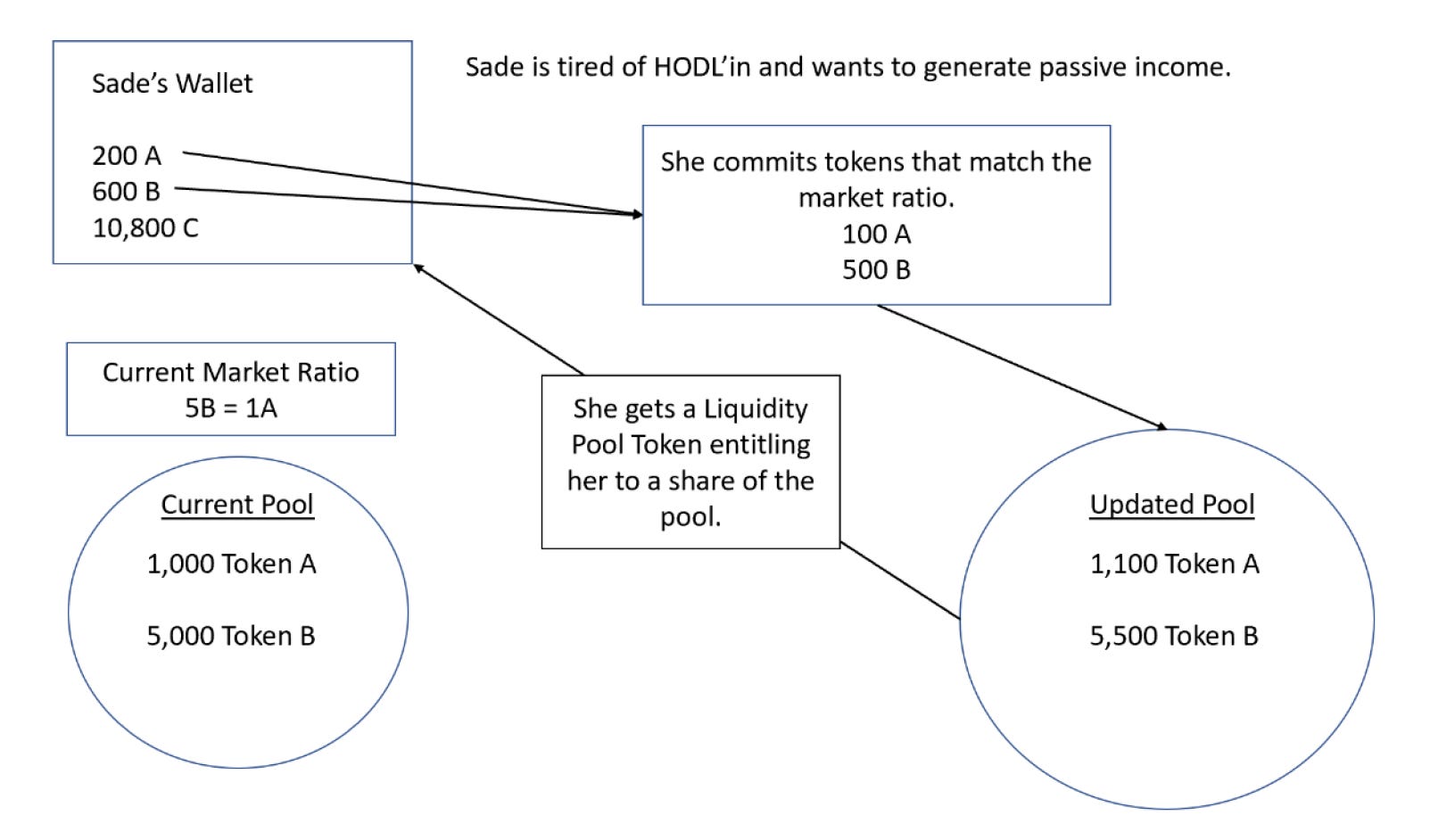

Taken from the Section II, Liquidity Pools of my book, Blockchain Thoughts and DeFi Economics. Sade puts some A and some B together, and adds it to a liquidity pool, her 11% share of the pool entitles her to 11% of the total swap fees. Those 0.3% fees are proportionally distributed to everyone providing liquidity. Giving your idle money the opportunity to generate additional value as a function of the trade volume. That is to say, if you have two popular tokens and people are switching between them a lot then you’re generating fees that are not capped by how much money you put in.

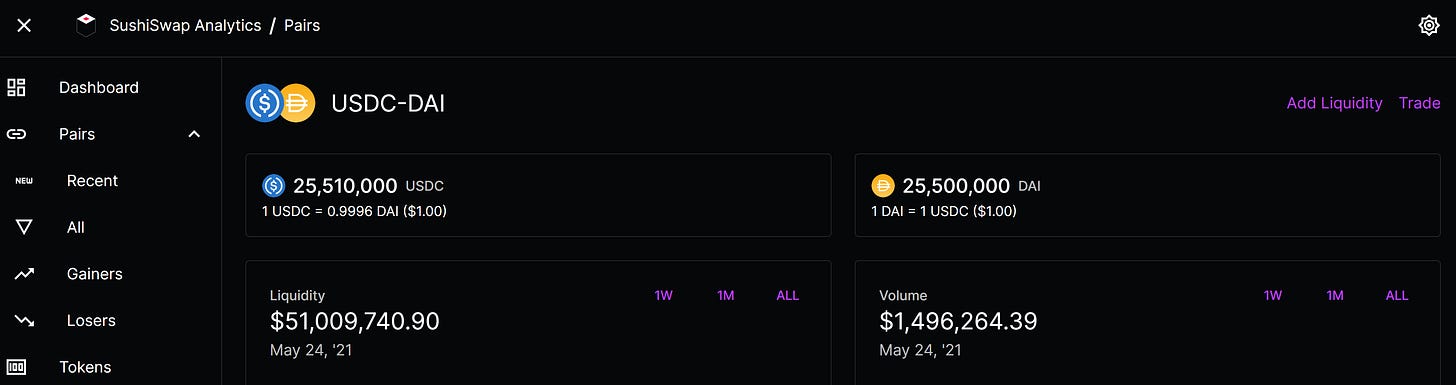

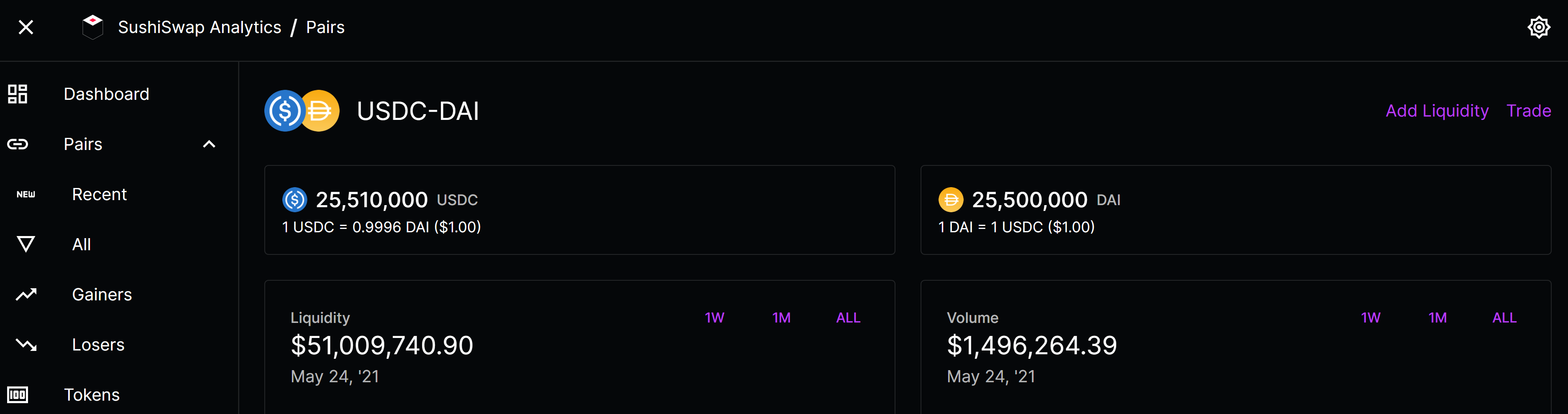

As a (complicated but bear with me) example. The Sushiswap USDC/DAI stablecoin liquidity pool on the Polygon Layer 2 network has $51M in liquidity.

So far on the day of the screenshot it’s had a trade volume of roughly $1.5M. The pool is lightly imbalanced (1 USDC = 0.9996 DAI, close to even but not technically as both coins fluctuate lightly around $1). 0.3% times $1.5M is about $4,500 (so far). This fee revenue is split between all liquidity providers.

Zapper, the “dashboard” of DeFi, estimates that this pool will generate 18% annualized returns given current liquidity and estimated future trade volumes.

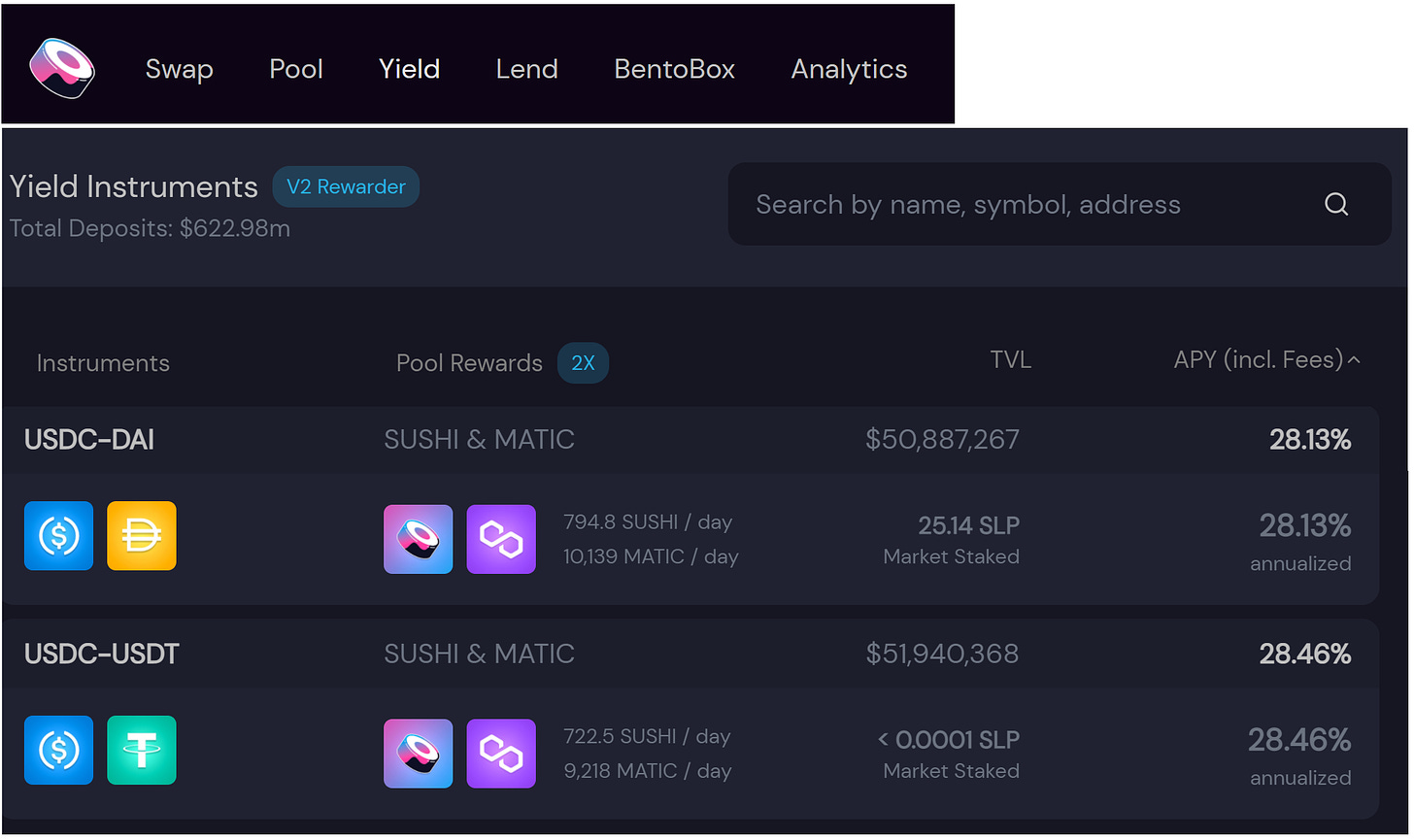

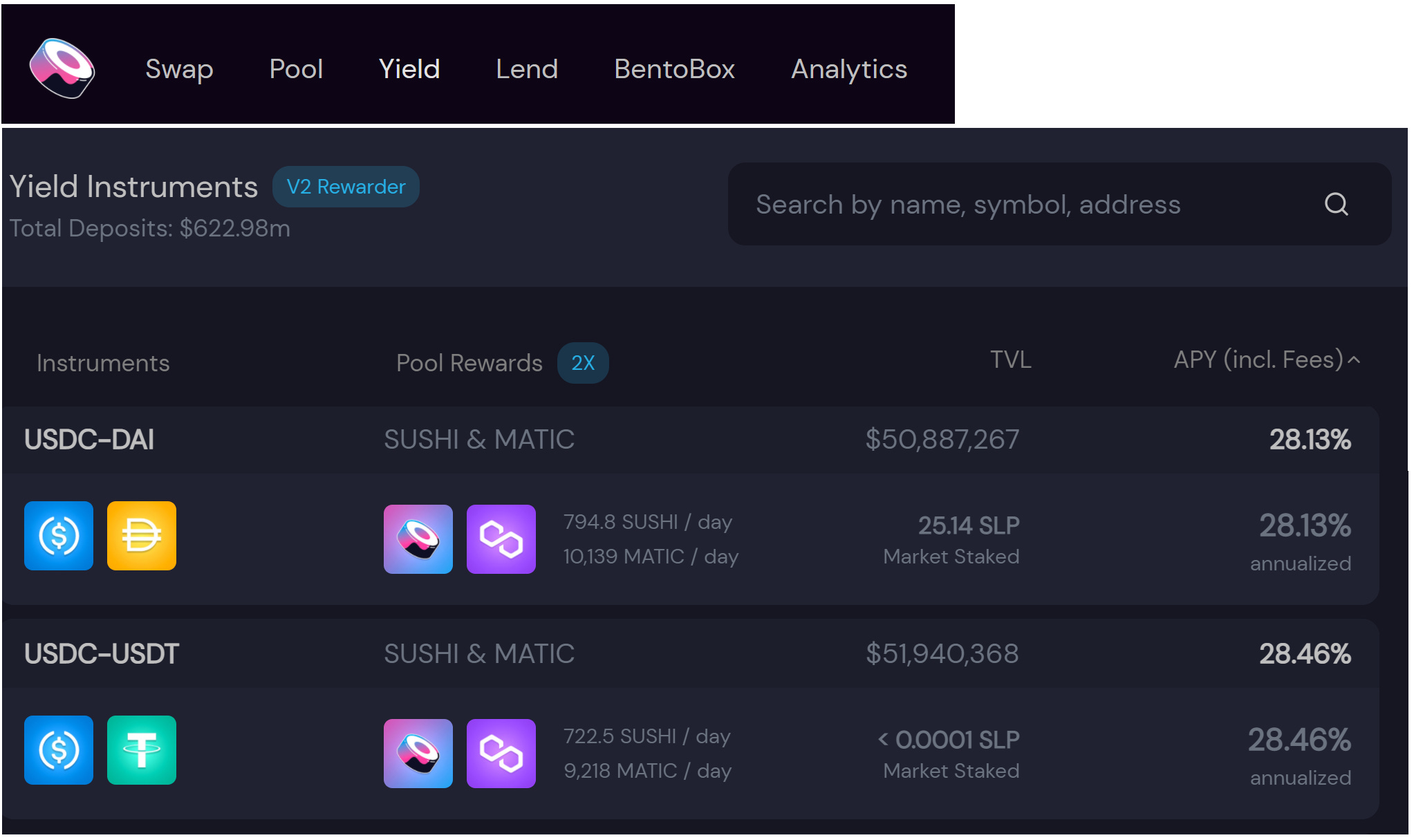

Screenshots taken while writing, the change in liquidity could be a lag or just natural fluctuations as people enter/exit the pool. Because liquidity is so important in DeFi, some protocols will add additional rewards as payment for bringing your liquidity to them as opposed to another protocol.

This is often called “yield farming” in the industry. Shopping your liquidity among the major exchanges to get the best benefits (both in rewards and in the trade volume / liquidity ratio that determines your fee revenue). Sushiswap is the most famous protocol for adding these incentives to bolster it’s growth plan.

Sushiswap will give you rewards in SUSHI and MATIC token for depositing your stablecoin liquidity pool tokens with them on the Polygon Layer 2 Network. Depositing your liquidity token with Sushi increases the estimated APY, but note, we've gone from 2 tokens (USDC, USDT) to 4 (USDC, USDT, SUSHI, MATIC) and the prices of SUSHI and MATIC are not stable. This APY may grow or shrink depending on their value. And of course, to do this, you have to trust them with your liquidity token. This adds additional risk. Generally speaking, if your liquidity pool token is incentivized at a major exchange, it is pure profit to let them give you rewards for it. But trust must be earned, do your own research!

Now this is where I give you a lot of caveats.

There are no guarantees. Typically what we’d expect is that liquidity chases ROIs, such that ROIs should converge to a market determined risk adjusted equilibrium. It’s possible a new exchange is giving insane incentives and people stop using your liquidity to make trades, reducing the trade volume (and your fee revenue!) tremendously.

Stablecoins are only as stable as their peg. Coins like USDT have had their share of regulatory scrutiny especially around whether there really is $1 behind that 1 USDT. Stablecoins are extremely revolutionary instruments in peer to peer exchange, but they still require trust in the centralized group that backs them.

There’s a lot of mechanics that I’ve skipped including how to even get stablecoins, how to put them somewhere that generates yield, how to get yield that returns enough value to pay the (unfortunately, very high right now) transaction costs to exit from crypto back to traditional finance profitably, etc.

I’ve skipped over a core concept: impermanent loss. Because stablecoins should perfectly correlate (stay at $1), impermanent loss is generally considered not relevant for stablecoins.

But for non-stable assets, this concept matters a lot. Because Liquidity pools automatically allow anyone to buy and sell from your pooled funds, realistically, they’re only going to do that when it’s profitable for them (i.e. buying something that is growing from you, and selling you something that is going down).

When coins are not stable the price movements of those coins can generate loss in excess of the fees recouped. This fundamentally counters my argument against HODLing. There are trackers out there that estimate the fees vs loss across liquidity pools to confirm providing liquidity is valuable.

I know this was a lot. The goal was to point out that stablecoins exist; that there are (relatively) low risk opportunities to generate non-speculation value in DeFi; that automated decentralized banks exist for borrowing/lending stablecoins; and that there are incentives to bring your liquidity (including stablecoin liquidity) to certain exchanges.

If you like this kind of writing you can subscribe & share!